Securities Trading Act (WpHG) Requirements Specification 2026

I. Introduction

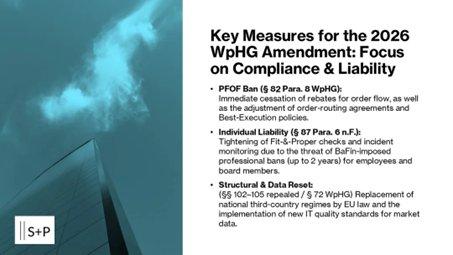

With the entry into force of the Act to Strengthen the Financial Center (StoFöG) on February 10, 2026, key provisions of the German Securities Trading Act (WpHG) were fundamentally amended. Of particular note are the prohibition of PFOF (Protection Against Unfair Financial Conduct) with penalty clauses (§ 82 para. 8 WpHG in conjunction with Art. 39a MiFIR), the expanded intervention powers of the Federal Financial Supervisory Authority (BaFin), including the possibility of professional disqualifications (§ 6 para. 8, § 87 para. 6 WpHG nF), new data quality requirements (§ 72 WpHG in conjunction with Art. 22b MiFIR), and the elimination of the national third-country regime (§§ 102–105 WpHG repealed; now MiFIR Title VIII). These amendments are complemented by adjusted penalty provisions (§ 120 WpHG nF) and new audit and reporting obligations (§§ 32, 89 WpHG nF). The following catalog of measures systematically operationalizes these normative requirements and prioritizes them according to risk intensity.

https://sp-unternehmerforum.de/compliance-seminare/

II. Implementation deadlines

With the entry into force of the Act on the Promotion of Financial Markets (StoFöG) on February 10, 2026, the German Securities Trading Act (WpHG) will undergo a fundamental reform to strengthen the financial center and align it with the MiFIR regime. For compliance, this means a complex transition phase with immediate prohibitions and staggered transition periods.

Particularly critical are the PFOF ban (§ 82 para. 8), which has been in effect since February 10, 2026, and the new professional bans of up to two years (§ 6 para. 8). While national third-country regimes were immediately abolished, the simultaneous elimination of best execution reports (RTS 27/28) provides administrative relief for institutions. Operationally, the new €200 million audit threshold (§ 32) only applies to financial years beginning after the cut-off date, meaning that audits for 2025/26 will still be conducted under the old regulations. Nevertheless, starting with the 2026 audit cycle , the new audit questionnaires (§ 89 para. 2) must be submitted on an ongoing basis, even if a full report is not prepared.

Key implementation deadlines of the 2026 amendment to the German Securities Trading Act (WpHG)

III. Requirements Specification 2026: Compliance, Money Laundering and Management

https://sp-unternehmerforum.de/seminare-geldwaesche/

The changes shift the focus from purely formal documentation to material effectiveness and individual responsibility .

1. Board membersand managing directors

The management bears ultimate responsibility for the proper organization of the business (§ 80 WpHG).

2. Compliance Officer (WpHG-Compliance)

The focus is shifting significantly towards data governance and behavioral monitoring.

3. Anti-Money Laundering Officer (AML)

Although the German Securities Trading Act (WpHG) primarily contains securities rules, the references to DORA and digital data tighten the AML obligations.

Status: Internal control document

Legal basis: WpHG nF, MiFIR, MAR, BMR

I. Compliance Officer (WpHG-Compliance)

Immediate measures (until the end of Q1 2026)

Short-term measures (until Q2 2026)

II. Money Laundering Officer (AML)

Immediate measures

Short-term measures

III. Board of Directors / Management

Immediate measures

Medium-term measures (until fiscal year 2027)

Sources:

Bundestag

S&P Unternehmerforum GmbH

Feringastr. 12 A

85774 Unterföhring bei München

Telefon: +49 (89) 45242970100

Telefax: +49 (89) 45242970299

http://www.sp-unternehmerforum.de

![]()